Micro-finance pools on Arbitrum are rapidly transforming access to capital in emerging markets, leveraging blockchain’s transparency and efficiency to drive meaningful financial inclusion. With Arbitrum (ARB) currently priced at $0.4191 and boasting transaction fees as low as $0.01 to $0.10, the network offers a cost structure that is 10,100x cheaper than Ethereum mainnet. This radically reduces the barrier for small-scale lending, savings, and investment products tailored for underserved communities.

Arbitrum Micro-Finance Pools: A New Paradigm for DeFi in the Global South

The adoption curve for Arbitrum micro-finance pools is steepest in regions where traditional banking infrastructure is fragmented or exclusionary. Recent metrics highlight surging DeFi activity in the Philippines, Nigeria, Brazil, and Indonesia, markets historically plagued by high remittance costs, limited credit access, and currency volatility. On-chain data from blockchain.news underscores how decentralized finance on Arbitrum is not just theoretical but actively reshaping economic participation across these geographies.

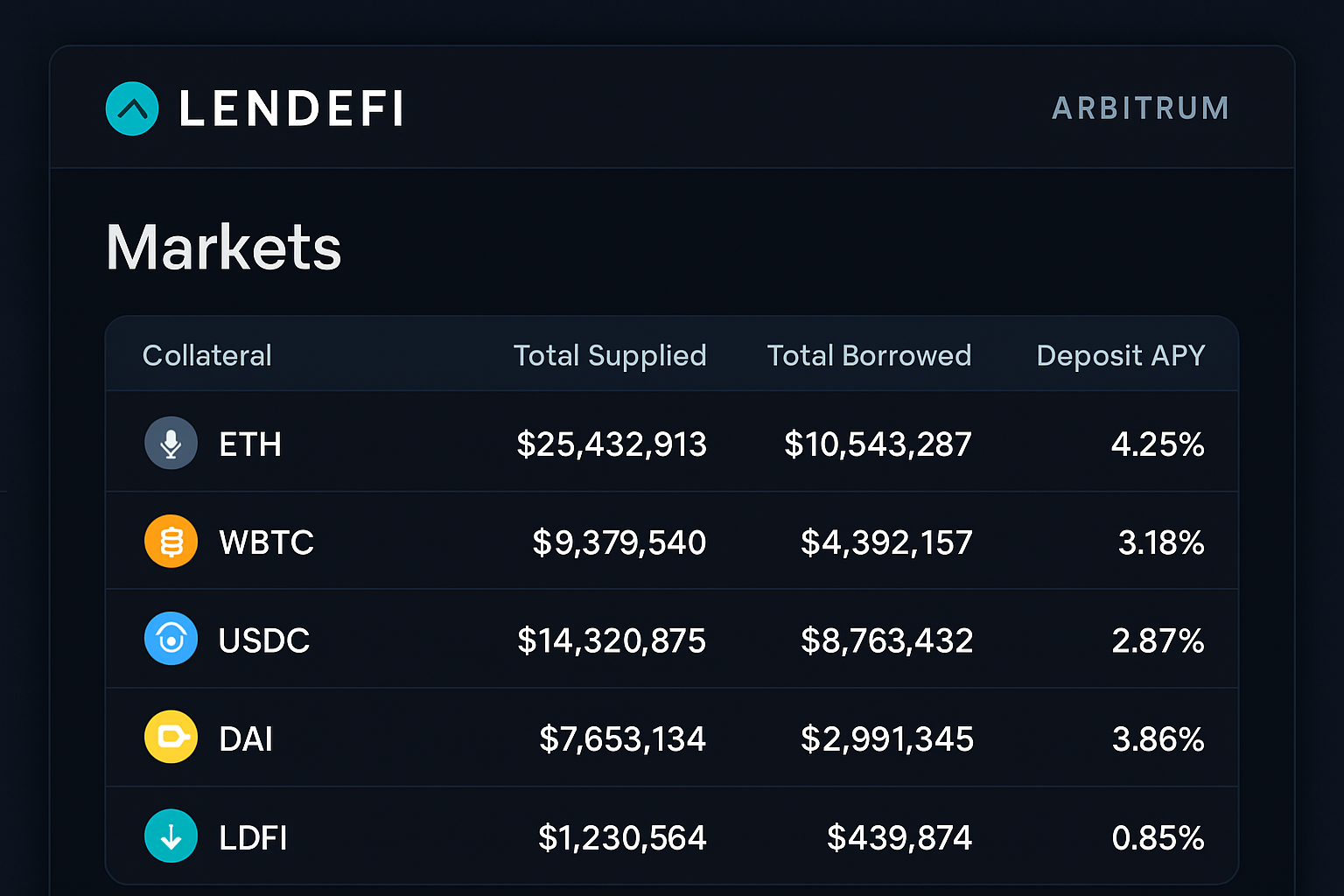

What sets these micro-finance pools apart is their permissionless nature: anyone with an internet connection can lend or borrow without intermediaries or credit bureaus. Protocols like Lendefi Markets exemplify this shift by enabling direct user participation in lending markets, no paperwork, no gatekeepers, just smart contracts automating everything from collateralization to repayment schedules.

Stablecoin Lending and Real-World Asset Integration: Expanding Access and Stability

The integration of stablecoin lending on Arbitrum has been a game-changer for volatile economies. Stablecoins such as USDC and DAI allow users to sidestep local currency devaluation while participating in global liquidity networks. Some protocols now offer stablecoin-to-stablecoin lending pools, ensuring near-stable borrowing costs even when fiat markets are turbulent (CoinLaw). The emergence of micro-escrow solutions further enables secure peer-to-peer transactions, critical for freelancers and SMEs operating across borders.

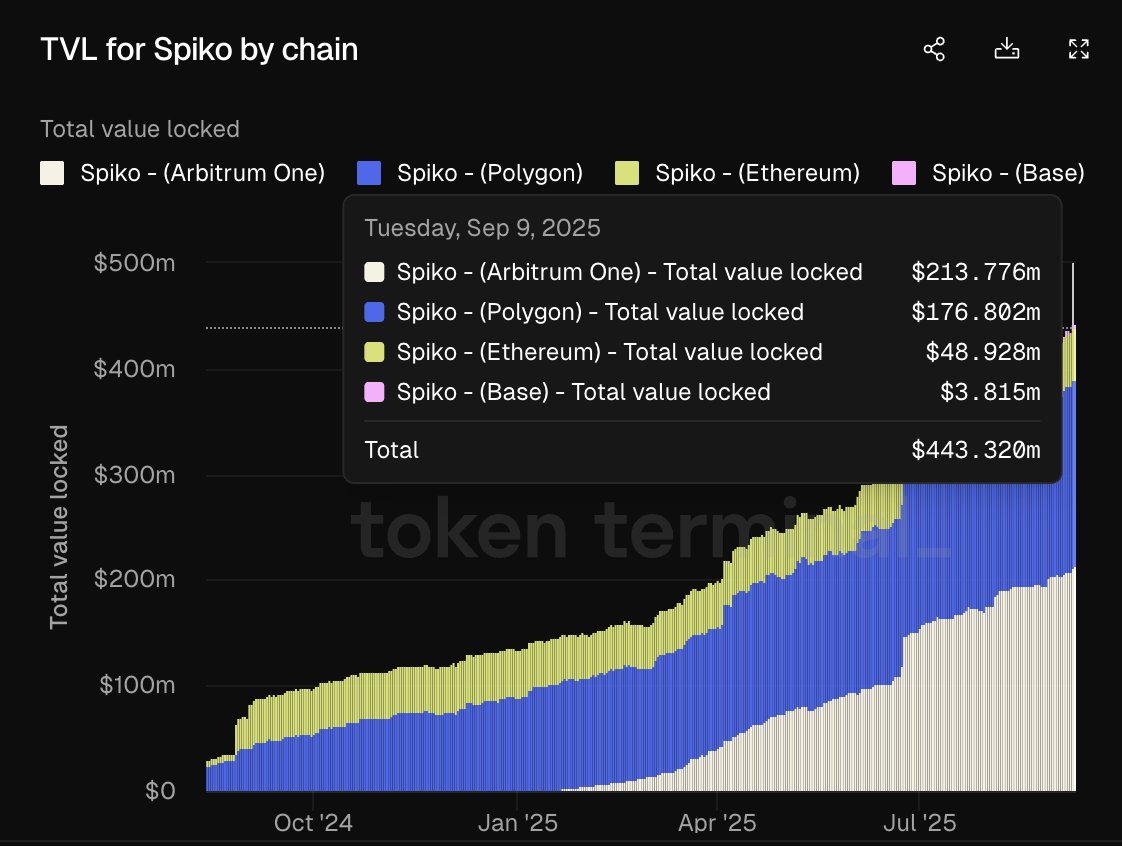

A groundbreaking development is the tokenization of real-world assets (RWAs) like Treasury Bills on Arbitrum via platforms such as Spiko money market funds (mikeroseresearch.com). By democratizing access to previously exclusive investment vehicles, these innovations empower individuals in emerging markets to diversify their holdings and hedge against local risks.

Comparison of Leading Arbitrum DeFi Protocols for Microfinance and Stablecoin Lending (2025)

| Protocol | Type | Key Features | Supported Assets | Minimum Transaction Fee | Emerging Market Focus | Unique Advantage |

|---|---|---|---|---|---|---|

| Lendefi Markets | Permissionless Lending | Microloans, no intermediaries, scalable pools | USDC, USDT, DAI, ARB | $0.01 | Yes (Philippines, Nigeria, Brazil, Indonesia) | Open market creation, low fees |

| Spiko Money Market | Stablecoin & RWA Lending | Tokenized Treasury Bills, stablecoin pools | USDC, Tokenized T-Bills | $0.01-$0.10 | Yes (Global South) | Access to real-world assets |

| Open Dollar | Stablecoin Protocol | Backed by LSTs & native tokens, stablecoin-to-stablecoin lending | USDC, LSTs, ARB-native tokens | $0.01-$0.10 | Yes | Stable borrowing costs, diverse collateral |

| Divine | Decentralized Credit | Liquidity pools, wallet integration, micro-credit expansion | USDC, USDT, ARB | $0.01 | Yes | $6.6M expansion for emerging markets |

| Uniswap V3 (Arbitrum) | AMM/Stablecoin Pools | Yield farming, micro-escrow, low slippage | USDC, WETH, UXLINK | $0.01-$0.10 | Yes | Popular pools for stablecoin access |

Permissionless Lending Platforms and On-Chain Credit Scoring: The Next Frontier

The expansion of decentralized credit platforms like Lendefi Markets onto Arbitrum signals a new era for DeFi emerging markets. These permissionless systems eliminate the need for traditional underwriters by using automated risk assessment models, often based on transparent on-chain activity rather than opaque credit histories. This approach not only slashes operational costs but also allows unbanked individuals to build digital reputations that unlock progressively larger loan amounts over time.

Arbitrum (ARB) Price Prediction 2026-2031

Forecast based on DeFi microfinance adoption, Layer 2 growth, and emerging market trends

| Year | Minimum Price | Average Price | Maximum Price | Year-over-Year % Change (Avg) | Market Scenario Insights |

|---|---|---|---|---|---|

| 2026 | $0.38 | $0.53 | $0.72 | +26% | DeFi adoption grows in emerging markets, but regulatory uncertainty and market volatility keep prices in a broad range. |

| 2027 | $0.47 | $0.65 | $0.95 | +23% | Expansion of real-world asset tokenization and microfinance pools drive higher TVL and user base. Potential for first bullish breakout. |

| 2028 | $0.61 | $0.82 | $1.18 | +26% | Mainstream integration of DeFi lending, increased stablecoin use, and improved UX boost adoption. Regulatory clarity emerges in key regions. |

| 2029 | $0.79 | $1.05 | $1.44 | +28% | Arbitrum cements its position as leading L2 for DeFi in emerging markets. Institutional interest grows, but competition from other L2s intensifies. |

| 2030 | $0.99 | $1.28 | $1.78 | +22% | Sustained DeFi growth, broader RWA adoption, and maturing microfinance ecosystem. Potential for cyclical market correction. |

| 2031 | $1.08 | $1.43 | $2.10 | +12% | Macro adoption slows but remains positive. ARB becomes a staple in cross-border microfinance and DeFi lending; market volatility persists. |

Price Prediction Summary

Arbitrum (ARB) is forecasted to experience steady growth through 2031, propelled by strong DeFi and microfinance adoption in emerging markets, real-world asset integration, and ongoing scalability improvements. While regulatory and competitive risks remain, the overall outlook is positive, with ARB potentially surpassing $1.40 on average by 2031 if adoption trends continue.

Key Factors Affecting Arbitrum Price

- Rapid growth of DeFi applications and microfinance pools on Arbitrum, especially in emerging markets

- Expansion of real-world asset tokenization and stablecoin adoption

- Launch of incentive programs (e.g., $40M DeFi DRIP) to boost ecosystem activity

- Improvements in user experience and lower transaction fees compared to Ethereum mainnet

- Potential regulatory developments influencing DeFi accessibility and compliance

- Competition from other Layer 2 solutions and new DeFi protocols

- Global macroeconomic trends and crypto market cycles impacting investor sentiment

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis. Actual prices may vary significantly due to market volatility, regulatory changes, and other factors. Always do your own research before making investment decisions.

The data speaks volumes: as more protocols integrate local currency rails and experiment with innovative forms of collateralization (from tokenized livestock to receivables), the addressable market for financial inclusion expands exponentially. However, challenges remain, technological literacy gaps, regulatory uncertainty, and crypto volatility all need thoughtful solutions before we see mass adoption at scale.

Projects like Divine, fresh off a $6.6 million expansion round, are scaling up their liquidity pools and wallet integrations to better serve emerging economies. This capital infusion is accelerating the deployment of user-centric DeFi applications built on Arbitrum, targeting the pain points of micro-entrepreneurs and informal workers who have historically lacked access to affordable credit facilities. The proliferation of decentralized lending dapps, now numbering 17 on Arbitrum according to Alchemy: signals a robust ecosystem where competition is driving innovation in yield optimization, risk management, and borrower onboarding.

One of the most promising trends is the rise of on-chain credit scoring. By leveraging transparent transaction histories and smart contract interactions, these systems can algorithmically assess creditworthiness without relying on traditional financial data. This not only democratizes access but also aligns with privacy-first principles, users control their data while still unlocking new opportunities. As these models mature, expect to see more granular risk-based pricing and dynamic collateral requirements tailored for the unique cash flow profiles found in developing economies.

Navigating Regulatory and Technical Hurdles: Sustaining Growth in DeFi Micro-Finance

The path forward is not without obstacles. Regulatory clarity remains elusive in many jurisdictions, creating uncertainty for both developers and users. The volatility inherent to crypto-assets also introduces risks that could undermine trust if not properly managed. According to the OECD’s recent analysis (OECD), successful expansion will require targeted education initiatives alongside robust consumer protections, especially as DeFi protocols begin integrating more complex real-world assets and local currency rails.

Key Benefits and Risks of Arbitrum Micro-Finance Pools

- Ultra-Low Transaction Fees: Arbitrum's average fees range from $0.01 to $0.10, making micro-transactions economically viable for users in emerging markets, compared to Ethereum mainnet's significantly higher costs.

- Increased Accessibility via Permissionless Lending: Platforms like Lendefi Markets on Arbitrum allow users to access microloans and lending services without intermediaries, reducing barriers for the unbanked.

- Access to Tokenized Real-World Assets: Projects such as Spiko's money market funds enable users to invest in tokenized assets like Treasury Bills, democratizing investment opportunities for individuals in emerging economies.

- Enhanced DeFi Ecosystem and Incentives: Arbitrum's $40 million DRIP DeFi incentive program boosts liquidity and user engagement, supporting the growth of micro-finance pools and yield opportunities.

- Exposure to Crypto-Asset Volatility: Users are subject to price fluctuations of assets like Arbitrum (ARB), which is currently priced at $0.4191 (as of 2025-09-29), posing risks to capital preservation.

- Regulatory and Compliance Uncertainty: The evolving legal landscape for DeFi and microfinance in emerging markets introduces risks related to compliance, user protection, and potential service disruptions.

- Technological and Educational Barriers: Limited digital literacy and access to reliable internet or smartphones can hinder adoption, especially among underserved populations.

Yet the momentum is undeniable. With Arbitrum (ARB) holding steady at $0.4191, network activity continues to climb as both retail users and institutional backers recognize the efficiency gains from Layer 2 scaling. The recent $40 million DRIP incentive program further underscores Arbitrum’s commitment to cementing its leadership in Ethereum L2 DeFi (MEXC). These incentives are already catalyzing new protocol launches and liquidity inflows, a virtuous cycle fueling broader adoption across continents.

Ultimately, Arbitrum micro-finance pools exemplify how decentralized technology can bridge persistent financial gaps at scale. By combining ultra-low fees, programmable risk frameworks, and borderless stablecoin infrastructure, they offer a blueprint for sustainable financial inclusion that adapts as user needs evolve. As regulatory frameworks mature and technical literacy improves across emerging markets, expect these protocols, and their impact, to grow exponentially.

No comments yet. Be the first to share your thoughts!