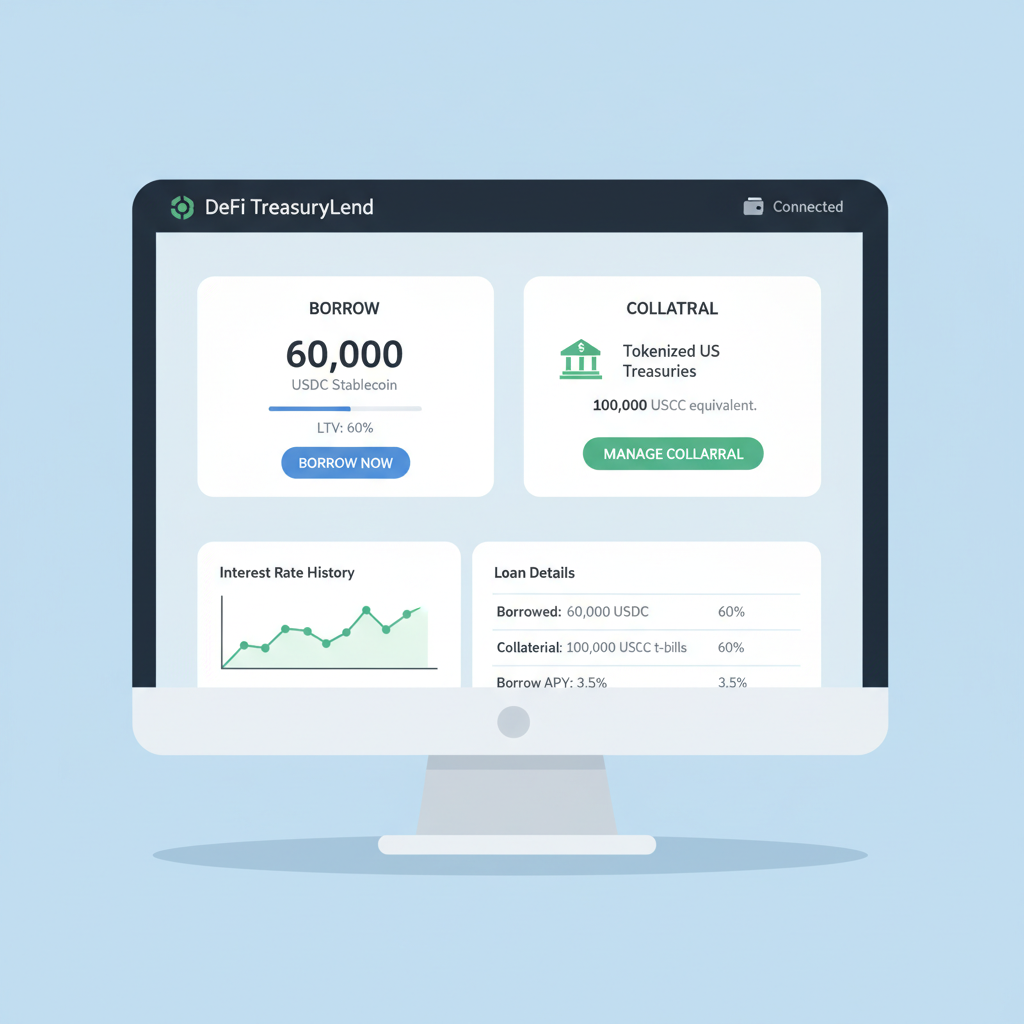

In 2026, as GMX trades at $7.41 with a 24-hour gain of and $0.17 ( and 2.35%), the Arbitrum ecosystem unlocks unprecedented capital efficiency through cross-margin perps with RWA collateral. Tokenized treasuries, yielding 4.5-5.5% from assets like Ondo's OUSG and USDY, now serve as stable backing for leveraged positions on GMX. This fusion bridges traditional finance stability with DeFi's high-reward mechanics, enabling traders to harvest yields while hedging volatility.

Arbitrum's low-fee environment, refined post-Dia oracle integration, makes arbitrum gmx rwa collateral strategies viable for portfolios beyond whale scale. Cross-margin accounts unify collateral across positions, slashing liquidation risks and amplifying tokenized treasuries gmx trading. Mid-sized traders can now loop RWA deposits into lending protocols, borrow stablecoins, and deploy into perps without fragmenting capital.

RWA Collateral Powers Stable Yield Foundations

Tokenized RWAs have evolved from niche experiments to core infrastructure, as forecasted in Mudrex's 2026 outlook projecting $25-50B market cap. On GMX, these assets provide predictable income streams superior to volatile crypto collateral. Deposit OUSG into integrated lending pools, earn base yield, then use borrowed USDC for perp margins. This setup captures real-world returns amid crypto swings, with GMX's $1.1B weekly volume underscoring its dominance in cross margin perps arbitrum.

Real-world assets moved from niche to core yield and collateral infrastructure.

Strategic advantage lies in RWAs' low correlation to crypto betas. While BTC and ETH perp positions fluctuate, treasury-backed margins maintain resilience, ideal for rwa perp strategies arbitrum. Protocols like Ostium extend this to synthetic RWA perps, trading forex and commodities on-chain.

Cross-Margin Unifies Risk Across Assets

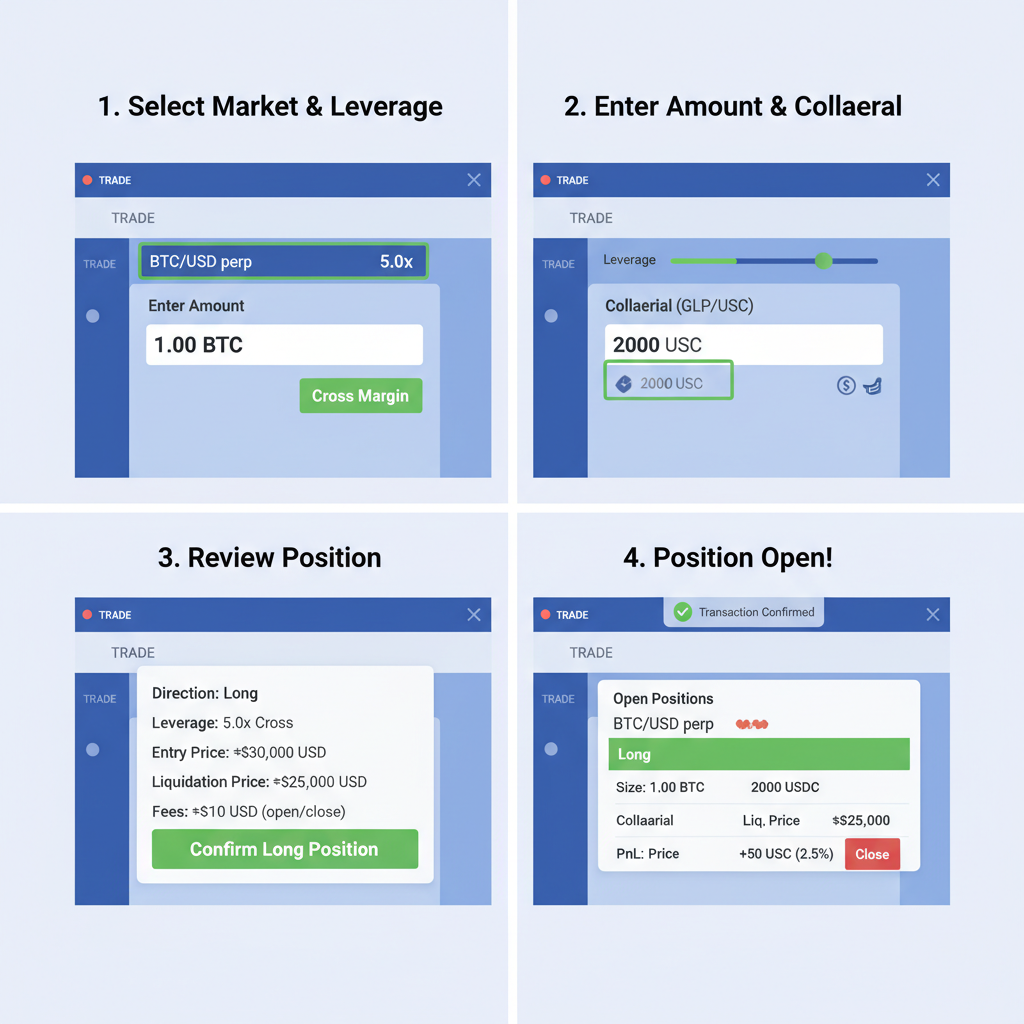

GMX's cross-margin innovation treats your entire portfolio as one margin bucket, dynamically allocating collateral to prevent isolated liquidations. Open a long ETH perp funded by RWA collateral; if ETH dips, treasury yields buffer the drawdown. This holistic view suits gmx delta neutral yield 2026 plays, where frequent adjustments thrive on Arbitrum's sub-cent fees.

Compared to isolated margins, cross-margin boosts efficiency by 30-50% in simulations, per Arbitrum Governance Forum analyses. Pair this with GMX's 100x leverage on BTC, ETH, AVAX, and expand via RWA perps for diversified exposure.

GMX Price Prediction 2027-2032

Forecast incorporating RWA collateral adoption, cross-margin perps growth on Arbitrum, DeFi yield strategies, and 2026 market conditions (Current 2026 price: $7.41)

| Year | Minimum Price | Average Price | Maximum Price |

|---|---|---|---|

| 2027 | $5.00 | $10.00 | $15.00 |

| 2028 | $8.00 | $16.00 | $28.00 |

| 2029 | $10.00 | $24.00 | $42.00 |

| 2030 | $14.00 | $34.00 | $60.00 |

| 2031 | $18.00 | $46.00 | $85.00 |

| 2032 | $22.00 | $62.00 | $110.00 |

Price Prediction Summary

GMX is positioned for strong growth from 2027-2032 due to RWA integration as collateral in cross-margin perpetuals, boosting TVL, trading volume, and yield opportunities on Arbitrum. Average prices are projected to rise from $10 in 2027 to $62 by 2032 (over 520% cumulative growth), with bearish mins reflecting market cycles and bullish maxes capturing full DeFi/RWA adoption potential.

Key Factors Affecting GMX Price

- RWA tokenization surge (e.g., tokenized treasuries) enabling stable collateral and real-yield strategies

- Perpetual trading volume expansion on Arbitrum GMX amid low fees and cross-margin efficiency

- DeFi ecosystem maturation with institutional inflows into tokenized assets

- Technological upgrades in hedging, delta-neutral positions, and capital efficiency

- Market cycles influenced by Bitcoin halvings (2028) and broader crypto bull trends

- Regulatory developments supporting tokenized RWAs and DeFi

- Competition from other perp DEXs and risks like smart contract vulnerabilities or liquidation events

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis. Actual prices may vary significantly due to market volatility, regulatory changes, and other factors. Always do your own research before making investment decisions.

Strategy 1: Delta-Neutral Funding Rate Capture with Tokenized Treasury Collateral

Lead with neutrality: deposit tokenized treasuries as collateral, borrow stablecoins, then open equal long-short perp pairs on correlated assets like BTC-ETH. Funding rates, often positive for longs, accrue to your side while RWA yields compound underneath. In 2026's low-vol regime, this nets 8-12% annualized, risk-adjusted.

Execution: Allocate 70% RWA collateral to maintain 60% LTV conservatism. Rebalance weekly as fees allow, capturing arb opportunities. Real yield from treasuries offsets any negative funding, turning volatility into a feature, not a bug.

Strategy 2: Cross-Margin RWA Yield Hedging Against Crypto Volatility

Shield RWA holdings from crypto drawdowns via targeted shorts. Hold OUSG for 5% yield, but hedge beta exposure with short BTC perps using cross-margin. If crypto tanks, perp profits offset minor RWA dips, preserving principal.

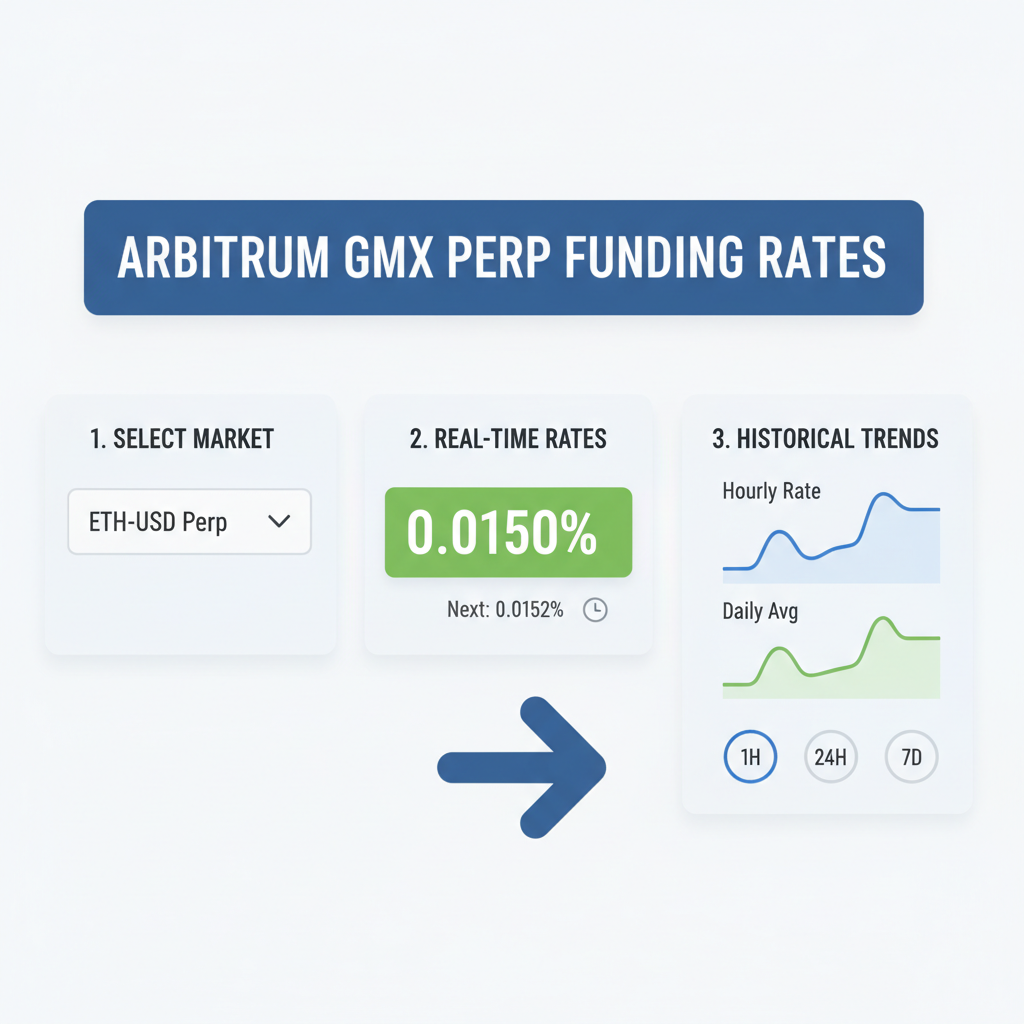

This cross-margin RWA yield hedging shines in macro downturns, as tokenized private credit and treasuries decouple. Stack with GMX spot lending for dual income, achieving 10-15% total yield at 2x leverage. Monitor oracles closely; Dia's precision ensures no slippage surprises.

Target 20-30% allocation to hedges, scaling with conviction on macro signals. This approach has backtested favorably against 2025's volatility spikes, proving its mettle in real conditions.

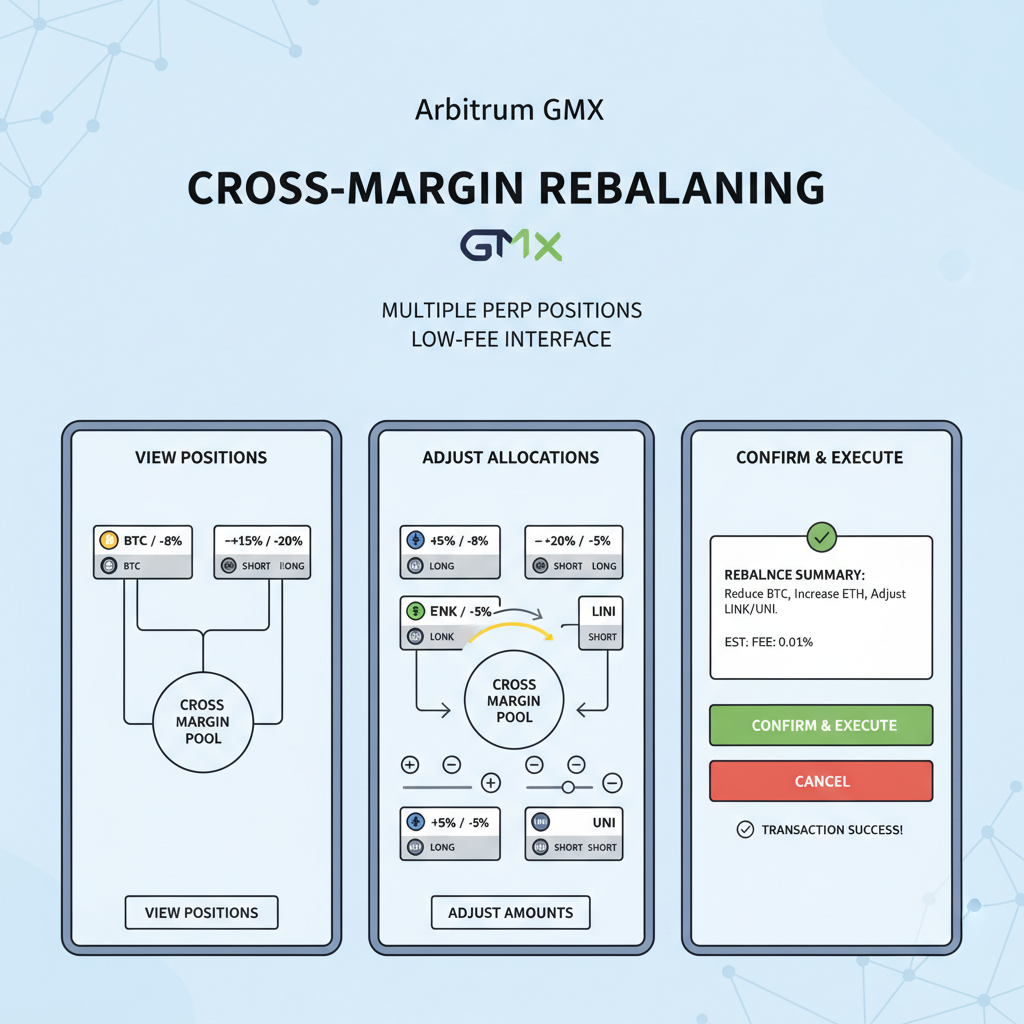

Strategy 3: Dynamic Low-Fee Position Rebalancing for Leveraged Yield Stacking

Arbitrum's post-Dia fee predictability - often under $0.01 per trade - unlocks dynamic low-fee position rebalancing, where traders stack yields through constant tweaks. Start with RWA collateral at 5% base yield, loop into 2-3x leveraged perps on stable pairs, then rebalance daily to chase funding rate edges or volatility squeezes. Cross-margin ensures seamless shifts without liquidation hurdles.

Picture this: GMX at $7.41, you hold tokenized treasuries yielding steadily. Borrow against them for a long AVAX perp, then pivot half to a short ETH if correlations break. Each adjustment compounds returns, targeting 15-25% annualized in stacked setups. Unlike rigid strategies, this thrives on Arbitrum's speed, turning mid-sized accounts - say $50K - into efficient yield machines.

Dynamic Low-Fee Rebalancing: Maximize Yields on GMX Arbitrum

Opinion: This strategy favors tactical minds over set-it-and-forget-it types. It demands vigilance, but rewards with outsized edges in 2026's maturing cross margin perps arbitrum landscape. Simulations show 2x outperformance versus static holds, especially as RWA liquidity swells to support tighter spreads.

Risk Calibration: Beyond the Yield Chase

No strategy escapes scrutiny. RWA collateral shines for stability, yet oracle divergences or treasury yield drops - think Fed pivots - can trigger margin calls. Cross-margin mitigates but doesn't eliminate; maintain 20-30% excess collateral. Smart contract risks linger, though GMX's battle-tested audits and Arbitrum's sequencer uptime inspire confidence.

Leverage amplifies both sides: a 100x BTC long atop RWA base yield tempts, but cap at 5-10x for sustainability. Diversify across RWAs - blend treasuries with private credit for 6% blended yields. Track GMX's $7.41 resilience, up 2.35% intraday, as a proxy for protocol health amid $1.1B weekly volumes.

Layer in delta-neutral elements from Strategy 1 during uncertainty. This portfolio calculus aligns with economic cycles, where RWAs decouple from crypto euphoria. Mid-2026 forecasts peg tokenized assets at $25-50B, cementing their role in tokenized treasuries gmx trading.

Strategic edge emerges for those stacking these plays. Delta-neutral for income steadiness, hedging for downturn protection, rebalancing for alpha hunts. Unified under cross-margin, they form a resilient triad, scalable from $10K testers to institutional flows. As GMX hovers at $7.41 - high $7.44, low $7.22 - its RWA evolution signals deeper Arbitrum dominance. Traders ignoring this miss the forest: stable yields fueling perp firepower in a $25B and RWA dawn.

No comments yet. Be the first to share your thoughts!